Plan members need the appropriate tools and education to navigate the path from employment to fulfilling retirement

Retirement planning in Canada requires a holistic approach, with individuals crafting a diverse portfolio to sustain their retirement years. The journey from employment to retirement requires a balancing act to navigate the intricate financial mechanisms involved. By equipping plan members with appropriate tools and education, this transition can shift from challenging to enjoyable. In this article, we delve into the multifaceted world of retirement planning for Canadian plan members who hold a mix of all three pillars of savings: government savings, workplace savings, and personal savings.

Understanding the three pillars of savings

Before diving into retirement income planning, it’s essential to understand the three pillars of retirement savings for Canadians mentioned above.

Pillar 1: Government programs

- The Canada Pension Plan (CPP): CPP is an earnings-based social insurance program in Canada that provides financial benefits as early as 60 or as late as 70, with annual benefits adjusted higher the later an investor starts taking payments.

- Old Age Security (OAS): OAS is a taxable and income-dependent benefit that provides a basic pension at 65 or as late as 70, with annual benefits adjusted higher the later an investor starts taking the payments, and it is subject to residency and post-18 years spent in Canada.

- Government Assistance Programs: Low-income retirees may also access additional benefits, such as the Guaranteed Income Supplement (GIS) or provincial income support initiatives.

Pillar 2: Employer-sponsored savings plans

- Many retirees benefit from employer-sponsored pension plans, including income from defined benefit (DB) or lump sum amounts in defined contribution pension plans (DCPP) or Group RRSPs.

Pillar 3: Personal savings and investments

- Individual savings accounts: Retirees often use RRSPs, TFSAs, and non-registered investment accounts to provide income during retirement.

- Rental properties: Some families accumulate wealth in real estate, generating income to support their retirement.

- Home equity: Homeowners can tap into property equity through downsizing, reverse mortgages, or home equity lines of credit to enhance retirement income.

Case Study: Larry and Brenda’s retirement plan

Meet Larry and Brenda, who are planning to retire next year. Larry’s employer has provided an opportunity to consult with a fee-based financial planner, so let’s dive into their key financial details.

Age: Both are 64.

Target retirement age: 65

Marital status: Married

Children: Two adult children, ages 28 and 30. Both live at home and work full-time.

Employment: Larry and Brenda are lifelong Canadian residents and are eligible for partial CPP and full OAS. Larry has been a hydro technician for 35 years. Larry’s employer offered him a DC pension, and he took advantage of this program. Brenda is an HR manager at a small firm, earning above YMPE. She took some time off work when their children were younger.

Retirement financial goals:

- Income: Larry and Brenda aim to generate a starting annual income of $80,000, adjusted for inflation, from various sources.

- Housing: They plan to live in their home as long as possible; however, they are open to the idea of someday downsizing to a smaller home or condo.

- Inheritance: Larry and Brenda would like to leave an inheritance for their children of at least $300,000 in today’s dollars, as they know that in 30+ years, that won’t buy very much.

- Lifestyle: Although they are both in good health, have a strong network of friends, and enjoy several hobbies, they haven’t given much thought to how they will spend their time in retirement. They have considered increasing their volunteering activities at various charities they have supported over the years.

Based on the above objectives and their current financial snapshot listed below, Larry and Brenda decided to invest as follows:

|

|

Financial snapshot |

Investment decision |

Projected Income |

|---|---|---|---|

|

Pillar 1 |

Both Larry and Brenda are eligible for CPP and OAS |

N/A |

Larry

Brenda:

These all rise with inflation. |

|

Pillar 2 |

Larry’s DC pension: $300,000 |

$200,000 is invested into a longevity risk-pooling mutual fund with a starting distribution yield of ~7%*

|

$14,000/yr. with distributions expected to rise (no guarantee)

|

|

$100,000 is invested into a fixed life annuity with guarantees but no inflation protection. The average of the providers equates to a yield of ~7% |

$7,000/yr. (guaranteed) |

||

|

Pillar 3 |

Larry:

Brenda:

Principal Residence: $1.2 million (no outstanding liabilities or mortgage) |

Both

|

Both

|

|

|

|

Total Projected Starting Annual Income: |

$83,000 |

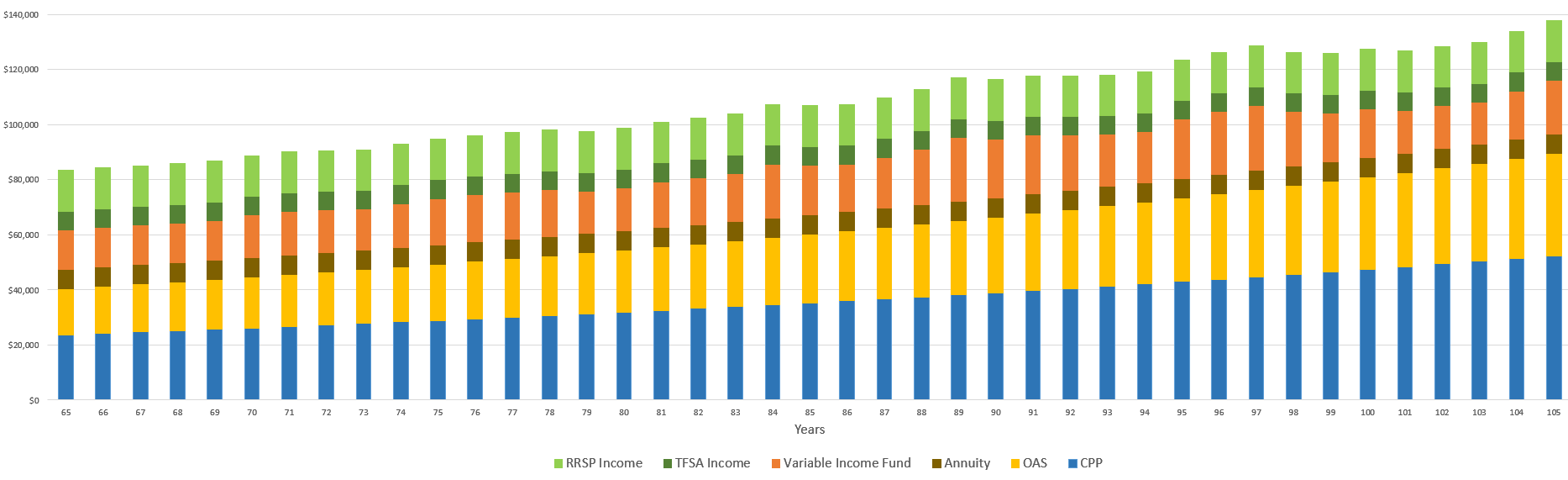

Larry and Brenda’s Retirement Income Picture**

Strength of Larry and Brenda’s retirement plan

- Income goals can be achieved: their projected starting income is slightly above $83,000, effectively meeting their income goal of $80,000. Still, regular budget reviews can help align their evolving income needs and resources.

- Their estate is protected: Their goal of leaving an inheritance is very likely to be achieved; they have flexibility between their assets and home to satisfy this goal.

- Longevity risk is mitigated: Their plan incorporates longevity risk protection via CPP, OAS, the longevity risk-pooling mutual fund, and the life annuity. The portion of their portfolio that lacks longevity protection has modest withdrawals (~4 percent); however, once they convert their RRSP savings to an RRIF, they will need to re-evaluate this strategy. As for the TFSA savings, only the interest is withdrawn. Again, there is flexibility built into their plan.

- Inflation is managed: Their plan incorporates inflation protection through CPP, OAS, and the longevity risk-pooling mutual fund, which is expected to increase distributions over time (but can go up or down any year.) From their other accounts, they will draw modestly to account for the likely higher income needs in the years ahead. Still, it’s important they observe the impact of inflation on their overall retirement expenses and revisit their plan as living costs change over time.

- Taxes are minimized: Their advisor has helped them minimize taxes and maximize after-tax income. In addition to using their tax-sheltered accounts thoughtfully, they incorporate income splitting and derive income from dividend-producing investments. They’re also taking advantage of savings within their TFSAs.

Other considerations

- Health care costs: While Larry and Brenda are currently in good health, they should factor in potential healthcare costs as they age. While some costs will likely go away as their retirement progresses, other spending may replace those items.

- Emergency fund: It’s essential for Larry and Brenda to maintain an emergency fund to cover unexpected expenses, such as medical bills or home repairs, without needing to dip into their retirement savings.

- Insurance: Reviewing coverage – including health and life insurance – is important to ensure everyone is adequately protected throughout their retirement.

- Social activities and hobbies: Retirement is not just about financial planning; it’s also an opportunity to explore new interests and enjoy life. They should take steps to stay engaged and fulfilled during retirement.

Conclusion

Larry and Brenda are fortunate they were able to accumulate the resources needed to achieve their financial and life goals in retirement. Working with their financial planner, they have made smart investment allocations around retirement income sources that reflect the full picture of their total assets. While they know they’ll have to revisit this plan annually as market returns unfold and their health and preferences evolve, this comprehensive approach adds resilience to maintain their financial security and help them enjoy a comfortable retirement.

Pat Leo is vice-president, longevity retirement solutions, Purpose Investments

*At the time of publication in September 2023, the Longevity Pension Fund yield to investors at 65 was approximately 7.00%. This figure is adjusted annually [ add full, proper disclaimer language]. For current yields, please visit: https://www.retirewithlongevity.com/fund/details-documents

** This example is for illustrative purposes only and is not indicative of expected nor guaranteed performance. In no circumstances should this be considered investment advice. RRSP (Registered Retirement Savings Plan) income is assumed to grow at 6% and drawn down by 4% annually. TFSA (Tax-Free Savings Account) is assumed to grow at 4.5%, which aligns with recent GIC (Guaranteed Investment Certificate) rates. The Longevity Risk Pooling Mutual Fund is represented by the Longevity Pension Fund, with a starting income rate of 7.16%. Distributions are based on the growth of $10,000 and total distributions received over the first 20 years, using the LifeWorks Economic Scenario Generator model—a dataset of 2,000 potential market outcomes—and align with the approximate 50th percentile scenario. Annuity income is fixed at 7.02%. Starting income for combined OAS (Old Age Security) and CPP (Canada Pension Plan) are $23,760 and $16,766, respectively, and are adjusted for 2% annual inflation